Investment

Is the Housing Levy a Good Investment for Kenyans? Economics Expert Analysis

Kenya Housing & Real Estate Analysis

Kenya’s Housing Levy and the Future of Affordable Housing

In 2023, the Kenyan government introduced the Housing Levy as part of its broader strategy to address the country’s growing housing deficit and accelerate the delivery of affordable housing. The policy immediately became one of the most debated economic reforms in recent years, generating discussion across households, employers, investors, developers, and the wider real estate industry.

While the initiative is positioned as a long-term mechanism for expanding homeownership opportunities, many Kenyans continue to question its structure, implementation, transparency, and long-term financial value. The levy represents more than a payroll deduction. It is an attempt to create a large-scale domestic housing finance system capable of mobilizing billions of shillings toward urban development and housing infrastructure.

What Is the Housing Levy?

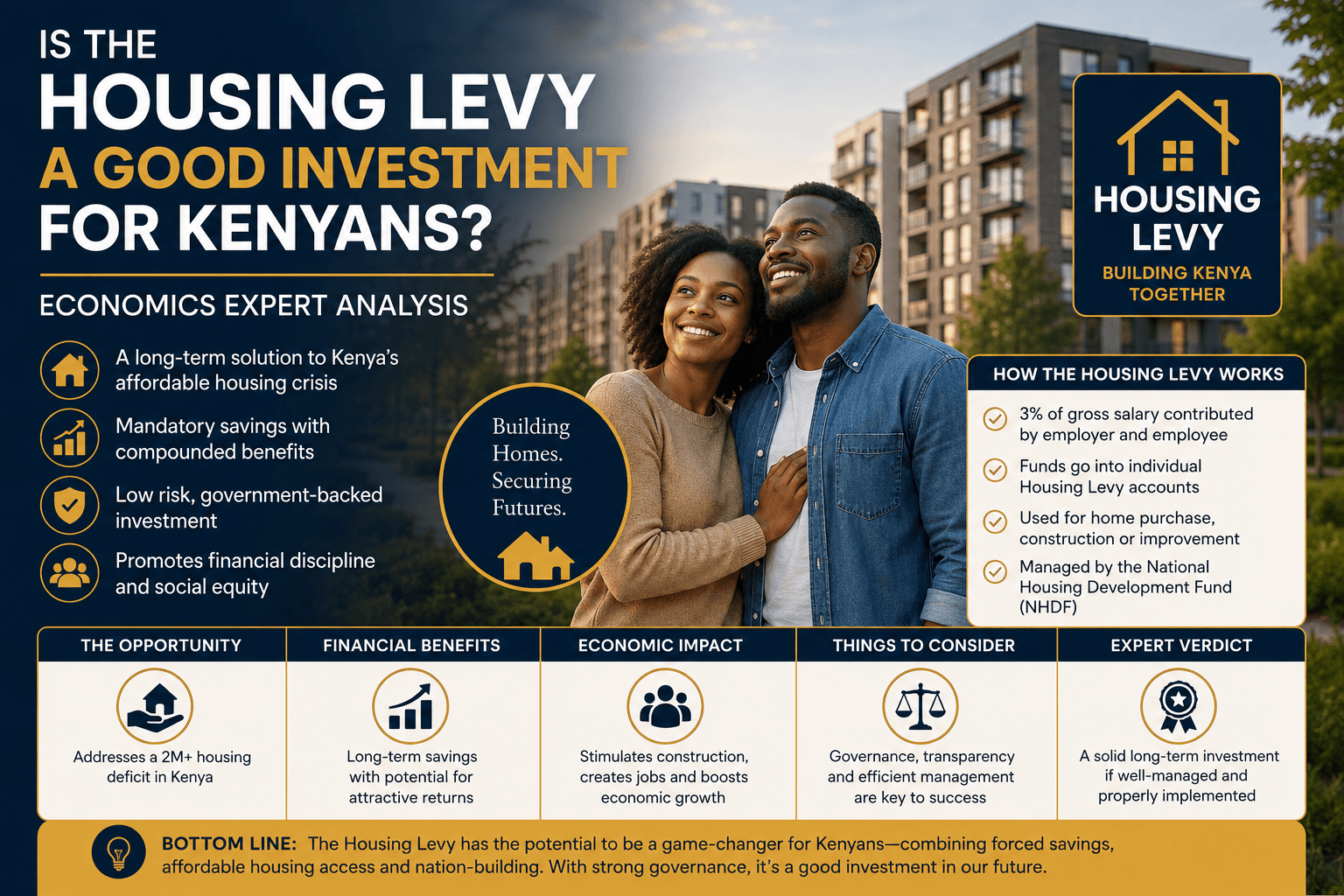

The Housing Levy requires employees in Kenya’s formal sector to contribute 1.5% of their gross monthly salary toward the Affordable Housing Fund, with employers providing an equal matching contribution. The collected funds are then allocated toward the financing and construction of government-backed affordable housing projects across the country.

The policy was introduced under the government’s affordable housing agenda and is closely linked to the Boma Yangu housing initiative. The broader objective is to create a sustainable funding structure capable of supporting large-scale residential development while simultaneously increasing access to affordable homeownership for middle- and lower-income earners.

At its core, the housing levy is designed to transform housing development from a purely private-sector activity into a nationally coordinated economic and infrastructure program.

Objectives Behind the Levy

Kenya’s housing deficit has been estimated at more than two million units, with demand continuing to rise due to rapid urbanization, population growth, and increasing migration into major cities such as Nairobi, Mombasa, Kisumu, and Nakuru. The Housing Levy was introduced as a mechanism to directly address this structural shortage while stimulating broader economic activity.

- Mobilize long-term funding for large-scale affordable housing development

- Stimulate employment opportunities within the construction and infrastructure sectors

- Reduce Kenya’s housing shortfall through accelerated residential construction

- Expand access to homeownership for salaried Kenyans under the Boma Yangu framework

- Create multiplier effects across financial services, manufacturing, logistics, and real estate sectors

Supporters of the initiative argue that affordable housing should be viewed as national infrastructure rather than a purely market-driven product. Under this perspective, coordinated public financing is considered necessary to unlock development at scale.

Is It a Good Investment for Individuals?

From an individual financial perspective, opinions remain divided. Contributors who intend to apply for affordable housing units through Boma Yangu may view the levy as a structured pathway toward eventual homeownership. Participation in the scheme provides contributors with prioritization during unit allocation and potentially improved access to financing.

However, for many salaried employees, the levy is often perceived as a compulsory deduction with uncertain personal returns. Questions continue to emerge around contributor benefits, refund mechanisms, allocation transparency, and ownership qualification criteria.

The long-term credibility of the housing levy will ultimately depend on whether contributors can clearly see measurable outcomes tied to their participation.

- Will contributors eventually own housing units directly linked to their payments?

- Is there sufficient transparency in the management and allocation of collected funds?

- What mechanisms exist for contributors who never qualify for affordable housing units?

- Will the program maintain long-term affordability relative to market pricing?

Real Estate Sector Impact

Despite public criticism surrounding the levy, the policy has the potential to significantly reshape Kenya’s residential real estate landscape. Increased access to centralized funding creates opportunities for larger-scale housing developments that may not have been financially viable under traditional market conditions.

Developers may benefit from more predictable project pipelines, while institutional investors could increasingly view affordable housing as a viable long-term asset class. The government’s role in aggregating demand and financing may also encourage new forms of public-private partnerships within the sector.

The Housing Levy introduces a more structured capital framework into Kenya’s affordable housing market, potentially accelerating residential development in both primary and emerging urban centers.

Beyond residential construction, the policy could increase demand across cement manufacturing, steel production, logistics, architecture, engineering, financial services, and urban infrastructure planning.

Economic and Investment View

Economists and policy analysts continue to debate the broader macroeconomic implications of the Housing Levy. Supporters argue that the policy represents an innovative approach to mobilizing domestic resources for infrastructure-led economic growth.

If implemented transparently and efficiently, the levy could generate significant multiplier effects throughout the economy. Increased construction activity may stimulate employment creation, expand manufacturing output, and strengthen demand across various supporting industries.

However, critics argue that the additional payroll deduction may reduce disposable income for employees already facing inflationary pressures and rising living costs. The policy therefore exists within a delicate balance between long-term infrastructure investment and short-term household financial strain.

Risks and Challenges

- Public concerns regarding transparency and accountability in fund management

- Resistance to mandatory contributions without direct contributor choice

- Legal disputes surrounding the constitutional interpretation of the levy

- Potential inefficiencies in housing allocation and project execution

- Long-term sustainability concerns if demand significantly exceeds delivery capacity

Ultimately, public trust will remain one of the most critical variables influencing the long-term success of the Housing Levy. Transparency, execution efficiency, and measurable delivery outcomes will determine whether the policy evolves into a sustainable housing finance model or remains a politically contested initiative.

Conclusion

Whether the Housing Levy becomes a transformative national housing solution or remains a controversial fiscal policy will depend heavily on implementation discipline, transparency, governance, and long-term economic outcomes. For Kenya’s real estate sector, the initiative introduces new capital flows and development opportunities that could reshape the affordable housing landscape over the next decade. For individual contributors, however, the debate continues around value, fairness, accessibility, and trust. As the program evolves, sustained accountability and measurable delivery will be essential in determining its long-term legitimacy and investment value.

Filed under

Related Reading

Murivest Community

Investor Discussion

Discuss investment opportunities, market trends, lease activity, financing, and underwriting with the Murivest community.

Join the Discussion

Share investment insights, market commentary, or leasing observations.

Professional discussion only. All comments are moderated.

Loading…

No discussion yet — be the first to contribute an insight.

Ask Murivest Research

Submit a Research Question

Questions on underwriting, leasing, market fundamentals, or capital structures are answered by the Murivest desk.

Murivest Research